Last week, the CRA announced changes to Form T661 (the tax form used to file SR&ED claims) that will be mandatory as of January 1, 2014. While the Income Tax Act remains consistent, the updated language on the T661 form requires claimants to disclose information in a new way. For the most part, it will not impact what can be claimed.

We want to highlight two of the major changes that we discovered as well as discuss the implications for your SR&ED claim (in our professional opinion, of course):

#1: Technical Requirements

We have consolidated former Sections B and C in Part 2 so that all claimants answer the same three questions in Section B. We have also changed the order of the questions in Section B.

What does this mean for your claim?

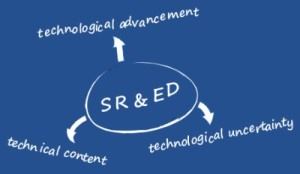

The consolidation of section B and C means that all claims, whether made for scientific research or experimental development, will have to address the same questions. In the past, Scientific Research claims had to answer only two questions as follows: “What advancements in scientific knowledge were you trying to achieve?” and “What work did you perform in the tax year, and how did that work contribute to the advancements described in Line 250?”.

The new form updated the wording and order of the technical submission. The updated section is now written:

[list list_style=”darkGrayDot”]

- What scientific or technological uncertainties did you attempt to overcome – uncertainties that could not be removed using standard practice?

- What work did you perform in the tax year to overcome the scientific or technological uncertainties described in Line 242? (Summarize the systematic investigation or search)

- What scientific or technological advancements did you achieve as a result of the work described in Line 244?

[/list]

The third question used the term “sought” instead of achieved and it was actually one of the first questions asked in this section. Based on our interpretation of this small, but very impactful, language change, the CRA is only looking to fund achievements achieved within the fiscal period. It leaves out the technological achievements sought but not achieved within the fiscal period. made in this particular fiscal year. On previous claims, applicants were able to list the overall goal over a longer time frame (possibly spanning multiple fiscal periods) In our opinion, this seems more restrictive on the eligibility and it will be interesting to see if the Research and Technology Advisors (RTA’s – CRA’s technical reviewers) take a different stance when reviewing the SR&ED qualifying work resulting in a decrease of successful claims.

#2: SR&ED Claim Preparer Information

We have introduced new Part 9 to capture SR&ED claim preparer information.

This change is fairly straightforward to understand: For the first time in the timespan of the federal program, the CRA is requesting information on who is assisting with the preparation of the technical and financial SR&ED information (whether an SR&ED consultant or accountant).

There is a strict penalty included on the form if any of this information is missing:

A $1000 penalty may be assessed if the information requested below about the claim preparer(s) and billing arrangement(s), is missing, incomplete, or inaccurate. Where a claim preparer has prepared or assisted in the preparation of this SR&ED form, the claimant and the claim preparer will be jointly and severally, or solidarily, liable for the penalty.

The CRA has confirmed in industry meetings that the information in Section 9 will be used to asses claim risk. This means that accountants and consultants which charge large fees above the industry average will be reviewed with more diligence.

Additional Changes

Other form changes, effective January 1, 2014, that we would like to highlight include:

[list list_style=”darkGrayDot”]

- Proxy overhead (one of two methods allowed to allocate overhead amounts associated with your R&D) will be reduced from 60% to 55%

- Can no longer claim capital expenditures or the right to use capital property

- Federal SR&ED rate for larger corporations will be reduced from 20% to 15%

[/list]

Now that you’ve had time to review the changes, how do you think this will impact your 2014 claim? Leave your comments and questions below, or contact us to discuss them in more detail.